SMM March 11 News:

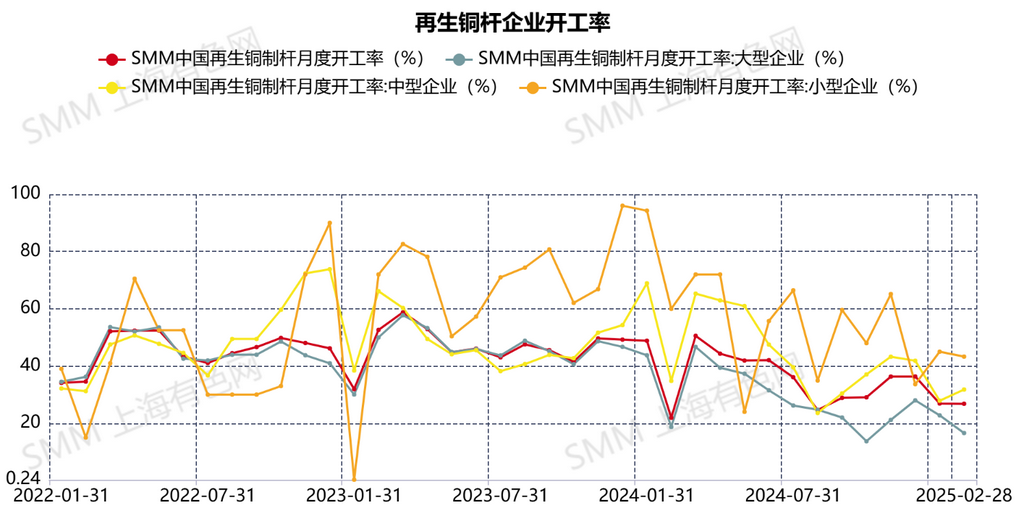

In February, the operating rate of secondary copper rod reached 26.81%, lower than the expected 31.7%. After the Chinese New Year holiday, copper prices initially rose and then fell, climbing to a high of 78,500 yuan/mt before pulling back to fluctuate within the range of 76,500-77,500 yuan/mt. Following the rapid post-holiday surge in copper prices, the price difference between primary metal and scrap quickly reached 2,800 yuan/mt, and the price difference between primary and secondary copper rods expanded to 1,370 yuan/mt. Although the economic benefits of secondary copper rods became apparent, end-users and traders remained cautious. Due to the further increase in copper prices compared to pre-holiday levels, post-holiday orders from end-user wire and cable enterprises were scarce, and restocking demand was slow to materialize.

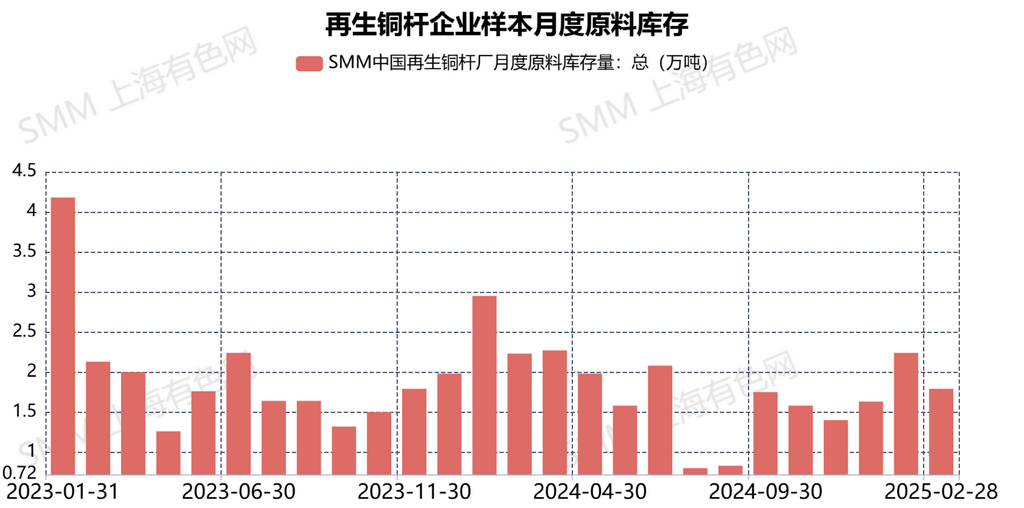

By mid-to-late February, high copper prices had fully suppressed downstream demand. Copper prices then pulled back, but the decline was limited. As raw material inventories at end-user wire and cable enterprises approached critical levels, they were forced to restock. However, given the limited order expectations, wire and cable enterprises maintained a just-in-time procurement strategy, considering active procurement only when copper prices fell to 75,000 yuan/mt. Due to the limited recovery in end-use consumption, the pullback in copper prices kept the price difference between primary metal and scrap hovering around 1,600-1,700 yuan/mt, while the price difference between primary and secondary copper rods narrowed to 700-900 yuan/mt. This dampened suppliers' willingness to pick up goods. According to interviewed enterprises, finished product inventories of secondary copper rods in February stood at 21,800 mt, down 4,000 mt MoM from January's 25,800 mt. With finished product inventories remaining at high levels, some secondary copper rod enterprises indicated that if finished product inventories continued to build up in March, they might consider temporarily halting production and resuming only after inventories decrease. Regarding raw material procurement, the rapid rise in copper prices before and after the holiday prompted many secondary copper raw material suppliers to offload large volumes of inventory, leading to low social inventories of secondary copper raw materials. Subsequently, the pullback in copper prices further tightened the availability of secondary copper raw materials. However, constrained by limited orders and the gradual nationwide implementation of "reverse invoicing," most secondary copper rod enterprises opted for just-in-time procurement, ensuring normal production was not affected by the tight supply of secondary copper raw materials.

Looking ahead to March, weak end-use consumption expectations have led many secondary copper rod enterprises to hold low expectations for the upcoming traditional peak consumption season. Most secondary copper rod enterprises anticipate that achieving 80% of the sales levels of the same period in previous years would be the best-case scenario.

In February, the raw material inventory of secondary copper rod enterprises was 17,900 mt.

The recovery of end-user wire and cable enterprises has been slow. According to interviewed data, post-holiday operating rates of wire and cable enterprises in south China were only around 40%, while those in east and southwest China were below 70%. Limited new orders, combined with high copper prices, discouraged secondary copper rod enterprises from purchasing excessive secondary copper raw materials. Additionally, as the month-end approached, local governments increasingly strengthened the enforcement of "reverse invoicing." More and more secondary copper rod enterprises fully adopted the "reverse invoicing" method in procurement, and the increased procurement costs led many enterprises to temporarily reduce their procurement volumes of secondary copper raw materials. They plan to make further procurement arrangements once the nationwide implementation becomes clearer. It is expected that secondary copper rod enterprises will maintain low raw material inventory levels in March.

The operating rate of secondary copper rod enterprises is expected to reach 33.49% in March 2025.

With the price difference between primary and secondary copper rods remaining below the advantageous threshold and wire and cable enterprises holding low expectations for the peak consumption season, many secondary copper rod enterprises have limited confidence in March production. Most secondary copper rod enterprises plan to maintain their current production schedules. Therefore, the expected increase in the operating rate in March compared to February is mainly attributed to the increase in workers' operating days.